A bank can lose money because it takes risks on its balance sheet, but what about a Fintech startup that only acts as an intermediary ?

I wrote in a previous article about the financial concept of Principal vs. Agent, and how disruptive finance has seen a lot of companies focus on being Agents, in other words push for Disintermediation.

A simple example of a Principal transaction would be a bank lending to a consumer – and therefore taking the risk of default. An Agent example would be a p2p platform connecting an investor to the borrower – and therefore NOT taking the risk of default, but leaving it with the investor.

Because the Principal (e.g. a bank) takes a credit risk and an Agent (e.g. a p2p platform) does not, it may seem that a Principal business model is much more risky than an Agent model. If I had asked “Can a Bank could lose $200m in one day ?”, the amount might have seen high, but not necessarily shocking because banks take Principal risk. But how could a Fintech company lose that amount if it only acts as an intermediary ?

Actually, we don’t have to look too far to see how it could happen – this is exactly what unfolded last week with the removal of the EUR/CHF floor.

Here is the background : (If you want an interesting summary of what happened, you can read this)

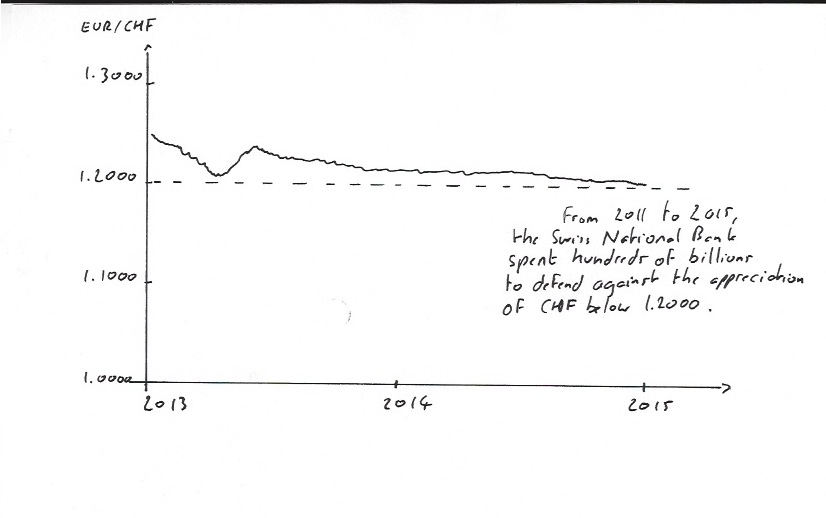

– In 2011, because of the European crisis, investors were scrambling for safe havens, buying Swiss Francs (considered as safe) and selling Euros (considered as risky)

– As a result, the Swiss Franc appreciated sharply, which made Swiss exports much more expensive, and put a strain on the Swiss economy

– The Swiss National Bank decided to put a stop to the Franc’s appreciation and declared a “floor” of 1.2000, effectively saying that a Euro could not be less than 1.20 Franc.

– Whenever the Euro risked breaching the floor, the SNB would sell CHF and buy EUR to push the exchange rate back up – they bought hundreds of billions of Euro assets since 2011.

For the last few years, the EUR/CHF exchange rate has therefore been very stable, hovering slightly above 1.2000 as can be seen from the following graph:

The EUR/CHF was stable for years

When an exchange rate has moved between 1.2000 and 1.2500 for years, and is trading at 1.2010, what would most investors do ? They would of course take the view that the rate would go back up to 1.2500 and take a EUR long / CHF short position – which is exactly what happened, with 90% of the market with the view that the EUR would appreciate vs. the CHF, and not fall below 1.2000.

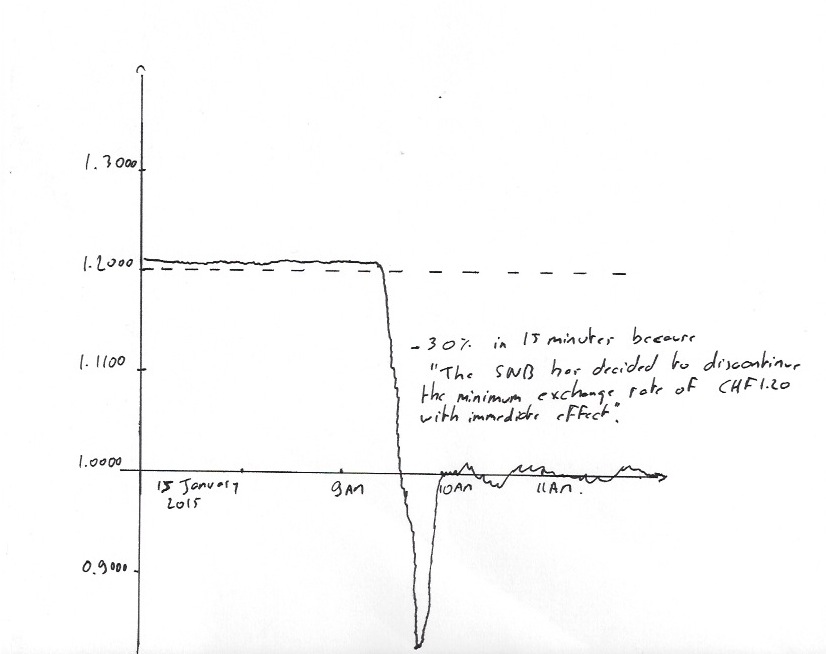

So what happened last Thursday ? The SNB took the market by surprise and declared that the floor was no longer necessary. What followed was the largest FX crash I have ever seen, with the Euro losing 30% of its value in 15 minutes!

In a matter of seconds, the EUR/CHF collapsed

Saying that a lot of investors lost money is an understatement. We have seen a hedge fund close because of its losses. Banks losing hundreds of millions.

But back to our question, how could a Fintech company lose money in such a situation ?

Let’s assume the following scenario :

– Let’s take a Fintech company involved in currency brokerage. By definition, it is an Agent, and all the risks are taken by its customers, not itself

– Say that I am a customer and take the view that CHF will depreciate. I take a position when EUR/CHF is at 1.2010, and hope that it goes higher. Let’s say I want to make CHF 1,000 gain when EUR/CHF goes to 1.2110 – not unreasonable looking at the graph. In order to mitigate the risk, my broker asks for CHF 1,000 of margin, so it’s protected if EUR/CHF goes down to 1.1910.

– Because I am prudent, I also put a stop loss at 1.1960, i.e. tell the broker to automatically cut my position if EUR/CHF goes below that level.

– So all is good, I’ll make a gain of CHF 1,000 if EUR/CHF goes back up to 1.2110, and make a loss of CHF 500 if it goes to 1.1960.*

What happens Thursday 15 January at 9:30AM ?

– The SNB says “bye bye floor, we don’t need you anymore”. Suddenly the 1.2000 line in the sand does not seem that relevant anymore. The market crosses that level in milliseconds.

– A few milliseconds later, my stop loss of 1.1960 is breached. My broker tries to close my position by selling EUR and buying CHF at 1.960.

– But nobody in the markets want to sell him CHF, everybody wants to buy CHF!

– My broker tries to buy CHF at 1.1900, 1.1800, 1.1700, 1.1600. Still no one. 1.1500, 1.1400, 1.1300, 1.1200, 1.1100, 1.1000, 1.0900, still no one. It continues until it finally finds a level at 0.8600!

– In other words, I have just lost CHF 35,000 on a trade where I thought I could lose CHF 500!

What happens to my broker (a Fintech Agent in a Disintermediation model…) ? In theory, nothing since I was the one who lost CHF 35,000. In practice, that’s not true at all, because the broker was suddenly hit by 3 different types of risk:

– It suddenly has a huge counterparty risk: whereas my broker knew that I could lose CHF 500 (because I had deposited CHF 1,000 of margin), the likelihood I can pay CHF 35,000 is suddenly much smaller. Even if it can’t collect CHF 35,000 from me, it still has to pay CHF 35,000 to the market counterparty that hedged its position. So my loss becomes my broker’s loss.

– It also had a settlement risk: many transactions that day were cancelled because trading systems went haywire. So my broker who thought that it had exited at a certain level might have lost much more than thought.

– And it was also impacted by the market risk, in case it had offered me a guaranteed stop loss. This is when my broker guarantees a stop loss at 1.1960 in exchange of a small fee. In that case, I would have lost only CHF 500, whereas my broker would have lost CHF 35,000.

These events did unfold in precisely that way last week, and we witnessed some FX brokers going bankrupt or losing hundreds of millions. We can argue that it was an exceptional event – which it was – but how many such “once in a lifetime” events have we witnessed during the last 10 years?

What does it mean for Fintech ? It means that a business can be impacted by financial markets, even if it’s an Agent in a Disintermediation model. We saw a similar phenomenon last year when dozens of p2p lenders in China went bankrupt – not because they were taking credit risk, but because their models could not withstand large defaults from their clients.

The truth is that any business, Fintech or not, will have risks. It just happens that Fintech companies will be more subject to risks from financial markets and this should be taken into account at the business model stage.

PS : thank you to Dan Dzombak for his comment on Twitter. As he righty pointed out, the currency broker is not just an agent, it’s also a principal because of the leverage it gives to customers. So there is definitely principal risk in there. But if instead of currencies (which are OTC, over the counter), I had considered equity indices such as the S&P 500 (futures traded on an exchange), or interest swaps, (that can be traded through a clearinghouse), then the separation between agent and principal becomes even more blurry – if not from a legal standpoint, but certainly from a risk standpoint. Which goes back to the point that even for a Fintech company, the risks are not always straightforward.

* Very simplified assumptions and calculations, just to give the idea of the trade.