One of the questions that often comes back when I talk about Disruptive Finance and Fintech is “What is the opportunity in Disruptive Finance ? “. This is clearly a question I’m also very interested in, and this article summarises my main thoughts.

Before answering the question, I think we should actually rephrase it. There is no doubt that technology will revolutionise finance. But consider the following : “The Internet will increase competition by making it easier for customers to compare prices, as well as by allowing new players to enter the market, since branch networks and other barriers to entry will become less important.” This was written in 1999 by the Riksbank1 ! 15 years later, where are the new players in banking ?

On the other hand, we can feel that some new financial sectors are emerging, e.g. p2p lending (see my previous article on the market size for p2p lending).

I think that the correct question should therefore be : Should you invest in Fintech TODAY ?

What is the opportunity in Disruptive Finance ?

My conviction is that technology will revolutionise finance, in the same way as it has revolutionised other sectors. Let’s consider a most extreme example :

– In 2013, 80.1% of music and video purchases in the UK were made online2. In other words, in less than 10 years conventional retailers saw their market shares drop from 100% to less than 20%…

– In the UK, online retailers are growing 6 times faster than conventional retailers3.

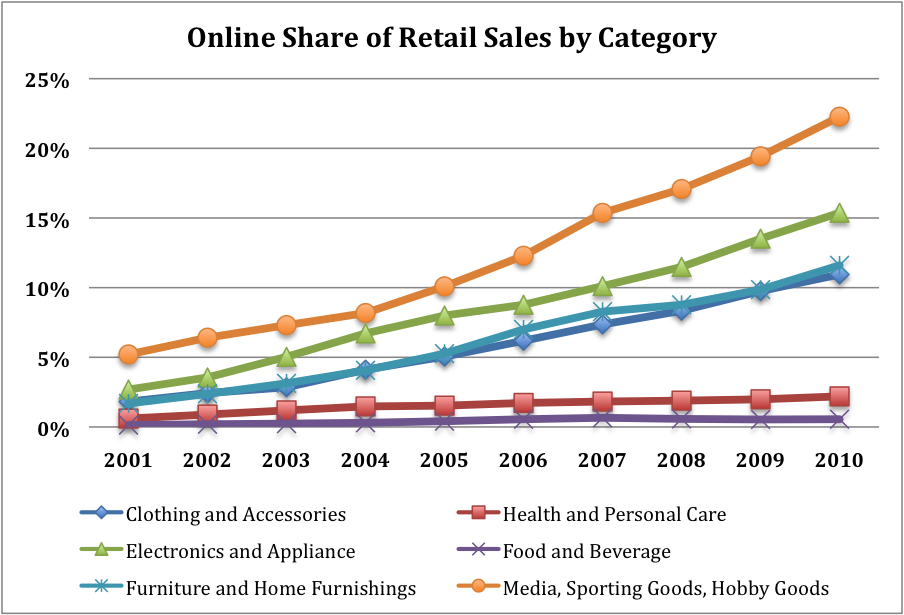

– This is not a trend that is slowing down : Ecommerce is quickly displacing brick and mortar as seen below

Online Share of Retail Sales by Category – With kind authorisation from Jeff Jordan

Note that we are not talking about a small obscure market, but about the whole retail market : Ecommerce has grown very quickly and is still growing very quickly – at the expense of conventional retailers. What about Disruptive Finance ?

For Disruptive Finance, a smilar analysis is more difficult because of the very wide areas covered by Fintech and Disruptive Finance. My opinion is that there are four areas to watch in Disruptive Finance :

1) The Incumbents and the Enablers

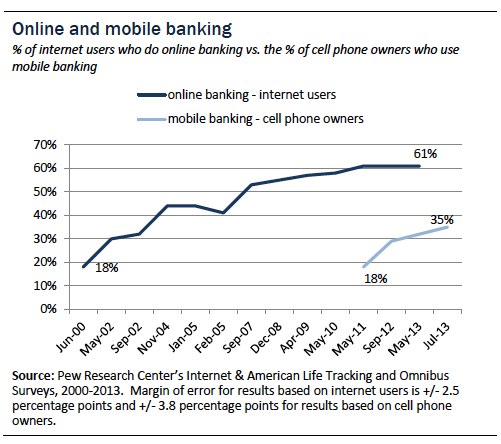

Incumbents – e.g. banks, brokers, fund managers – have clearly added a digital channel to their offering, which allows for example their clients to access their accounts online, or transact on their mobile phone. This is a trend that started 10 years ago and is now standard as evidenced by the data from Pew Research below – two thirds of Internet users use online banking. Together with this growth in digital channels, companies that enable this digitalisation process have therefore grown strongly. It is therefore not a surprise that in the Fintech 100 of American Banker, 8 of the Top 10 Fintech companies are involved in IT Services.

Growth of online banking – With kind authorisation from Pew Research Center

Investing in the incumbents can be difficult – because their business includes much more than just Fintech – but clearly many banks have identified the new opportunities brought by technology and are transforming their business accordingly*. But investing in enablers should definitely be an option. Why today ? Because the process of digitalisation is still far from complete…

* For obvious reasons, I will not elaborate about the various models of different banks

2) The New Players

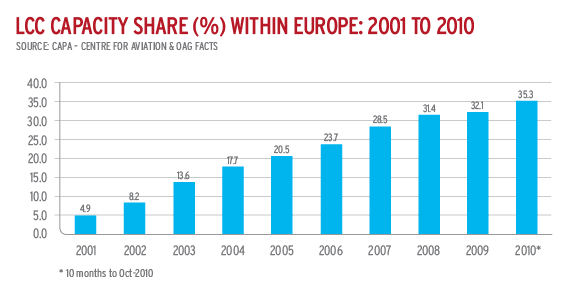

By definition, incumbents need to build from an existing model, whereas new players – pure players – can start from scratch with a different value chain. Low Cost Carriers in the airline industry represent a good example of an industry that was revolutionised – with LCCs taking more than a third of market share in Europe in less than 10 years.

Market share from Low Cost Carriers in Europe – With kind authorisation from Airline Leader

I would argue that we haven’t seen such disruption from new players in Finance yet, but that some tentative disruption is emerging. For example :

– Simple (acquired by BBVA) or Moven as a no frills Internet banks – a smarter version of the LCC applied to banking

– Kabbage and Ondeck as data-driven SME banks – the vision of a bank with real-time credit analysis

– Wealthfront and Betterment as no frills investment platform

– Etc..

Investing in The New Players should definitely be considered, but these companies are usually much smaller – this means Venture Capital. What about timing ? This is worth investing in the companies that are already showing exponential market adoption.

3) The Real Disrupters

In this category, we would have the Amazons of Finance, the revolutionary business models that do not exist yet. The graph below shows the very interesting dynamic between a Disrupter and an incumbent, in that case Amazon vs. BestBuy. Note that in 1998 BestBuy had revenues of $10bn when Amazon started at zero. Amazon grew very fast, but BestBuy also continued to grow – until BestBuy came to a sudden stop in 2009, with Amazon still growing. The latest figures of 2013 show BestBuy now much lower (around $40bn) vs. Amazon at $75bn – almost double !

This is the main characteristic of real disrupters – they start from a very low level, grow quickly, but are still considered as too small to be a threat, until they really cannibalise demand from incumbents.

")

From Bloomberg

Today, we would have in this category different companies such as :

– Lending Club, Prosper, Zopa, Funding Circle, etc. : p2p finance as a way to disintermediate incumbents

– Bitcoin, Litecoin, etc. : digital currencies to replace the current monetary system

– Square, Dwolla, and let’s not forget Paypal : digital payments

– Etc…

Investing in the Disrupters should definitely be part of an investment process in Disruptive Finance. Again, this is usually at the level of Venture Capital. What about timing ? Now is a good time when some areas (i.e. p2p finance) have gone from 0% to 2% of the whole market in a couple of years.

4) The Outsiders

Do you remember Nokia ? In 2007, Nokia had a 40% market share. Together, Nokia, Samsung, Motorola, Sony Ericsson and LG had a market share of 85%. In 2007, Apple launched the first iPhone. Apple was clearly not a small company, but had by definition 0% market share in mobile phones. Fast forward 6 years, Apple captures more than 50% of all the profits in the mobile phone industry – and everybody else except Samsung loses money in that sector !

Who will be the outsiders ? For as long as I remember, Telecom operators were seen as a threat to banks and payment systems. It is fair to say that it hasn’t happened yet. More generally, all companies with a very large customer base could pretend to disrupt financial services. For example :

– Telecom operators : although it hasn’t happened yet, Vodafone shows how it can be done with M-Pesa having more users than all local banks combined in Kenya. And this is arriving in (Eastern) Europe…

– Portals and e-commerce sites : Alibaba launched a competing offer to savings accounts, and got 80m new clients and $80bn new money in 9 months…

– Etc…

Investing in the Outsiders is not necessarily easy though – the impact of Disruptive Finance on their business will always be small to start with, until the day when it is not… Although Alibaba has had a stellar growth in Finance, investing in Alibaba today means paying for the rest of the business, not really its financial offering…

PARTIAL CONCLUSION

Is there an opportunity in Disruptive Finance today, and can technologies revolutionise Finance ? Clearly Yes.

Is it happening now ? My answer is also Yes.

What would be the best way to invest ? That would depend on the objectives.

– If the objective is to find a sector that will grow strongly over the next few years with a good likelihood, then investing in the Enablers can make sense

– If the objective is to replicate the success of the Low Cost Carriers in Finance, then investing in the New Players could be interesting

– If you want to find the next Amazon of Finance – with all the risks that come with it – then Venture Capital and investing in the Disrupters is the key

– And let’s not forget all the existing Outsiders, the Vodafone and Alibaba of this world – but the investment proposition might be more challenging.

WHAT ABOUT TIMING ?

Why do I keep insisting on timing ?

Let’s go back to the question : should you invest in Fintech NOW ? To answer YES, we would need to answer the two following questions :

1) Are disruptions happening in Finance now ? I believe the answer is YES

2) Can you invest in the opportunity at a reasonable price ? This is less clear…

Consider the following example :

– In 1999, you – rightly – identify Online Travel as a huge opportunity. You also believe that the first-mover advantage of Expedia, Travelocity and Priceline will help them dominate that market. Again, you were right, these 3 companies are still dominant 15 years later.

– In 1999, you invest in Priceline at a valuation of $20bn. Today, they are worth $60bn – it is an OK result, but not great considering you managed to pick both a winner and a growth industry 15 years down the line.

– Moreover, would you have kept your investment in Priceline when its valuation was divided by 100 to $200m in 2001 ? And would you have waited 10 years to see it come back to $20bn ?

This is exactly what worries me – picking the right investment in the right industry, but at the wrong time. I witnessed both the Internet bubble AND the subprime crisis as an insider. The first time, I had not idea, and was happy enjoying the bubble like everyone else. The second time, with more experience, I saw it coming and advised to protect against it. What about today ?

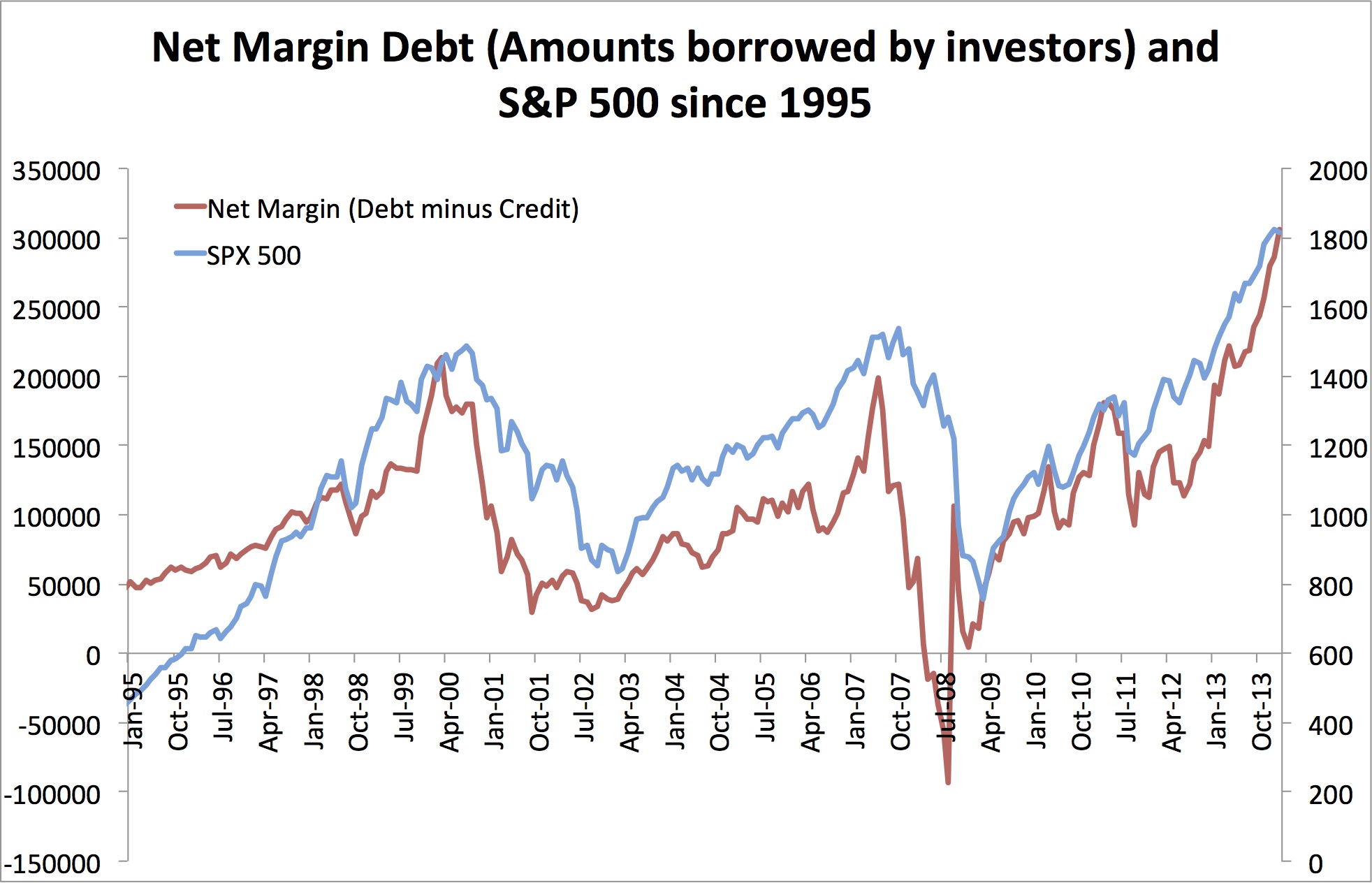

From NYSE (Net Margin Debt) and St Louis Fed (S&P 500)

The graph above shows the amounts borrowed by investors. It is a way to spot bubbles – that happen not only when investors borrow more and more to buy equity on margin, but also when the speed of borrowing increases very quickly. We can observe the bubble frenzy of 2000 and 2007. Leveraging is important, because when markets fall, leveraged investors need to cut their positions because of margin calls, which pushes markets down, etc. Today, investors are clearly leveraging more, but the speed of leveraging hasn’t yet reached the levels of 2000 and 2007. Observe also that leveraging falls before any big S&P decline

I could spend hours and show a countless number of graphs to discuss the current market environment, but the important take away for our discussion is the following :

– The market is not far from a bubble environment, with a risk of a severe crash

– This is however not guaranteed – because a correction could bring market conditions back to a more normal environment

With this in mind, it makes the investment case for Disruptive Finance very challenging :

– Huge business opportunity

– But very expensive and risky, making the risk/reward less attractive

What shall you do in such an environment ? I see two clear strategies :

1) If money is falling from the sky, and the business opportunity is huge, it’s the best time to be an entrepreneur ! You will clearly face some competition, but a good team with a good understanding of both technology and finance could do wonder.

2) The second option is to start investing now – even if it is risky and expensive. Because risky and expensive does not mean that it cannot be more expensive* – especially if it is the next Amazon of Finance… The risks can be mitigated through a thorough analysis of comparables, and by keeping plenty of cash available to invest in an eventual correction – remember buying Priceline at $200m…

*Not mentioning other macro scenarios, such as inflation, etc. that are outside the scope of this blog.

CONCLUSION

Disruption is happening in Finance NOW. Because Incumbents will adapt, Enablers will thrive. New Players will also emerge. At the same time Real Disrupters are being created and some Outsiders will grab a slice of this new market.

Nothing is certain in Finance, but there is a risk that we are in a bubble. The best way to benefit from a bubble is to be an entrepreneur and raise as much money as possible – in order to have enough cash to build the business. For an investor, it still makes sense to invest but it is important to get the figures right and keep a lot of spare cash available.

This is my opinion on the current opportunity in Disruptive Finance. Do you agree ? Don’t you agree ? I’d love to have your views, send me a message.

1 Riksbank, Structural Changes in the Banking Sector, 1999

2 SAS, How the UK will shop, 2012

3 Center for Retail Research, Online Retail : Europe, the UK and the US, 2014