My thesis has long been that technology would have a huge impact in finance, but that it wouldn’t be a linear process. Let’s summarise where we are in this transformation of finance:

- 2013 onwards: huge enthusiasm in Fintech and the vision that tech would transform finance with disruptors challenging traditional companies. My view at the time: vision is right, but it would take more time than people expected, because infrastructure and consumer behaviour not ready yet.

- 2016 onwards: the peak of the Fintech bubble? Fintech becoming more institutionalized and being seen as enablers for large institutions rather than disruption – the recurring concept being collaboration between large organisations and startups. My view: this is the beginning of real disruption with the rise of new financial products and usages. Think of the advertising world before and after Google: the Googles of finance are happening now.

As Fintech has become more institutionalized, as many of the early innovative concepts such as peer-to-peer lending or crowdfunding have lost steam (at least in the news cycle), it feels that the big Fintech bubble has become a boring IT play, where it’s less about disruption, and more about optimization of existing processes.

It seems that the big Fintech tsunami has become an IT infrastructure ripple.

I disagree.

The $50bn of investments in the last few years have laid the foundations – in terms of infrastructure, talents, technology, but more importantly consumer behaviour – of dramatically new business models in finance, which I would summarise with one word : hyperscalability.

Let’s take a step back and analyse the way different types of companies normally grow.

- Traditional financial companies scale over decades and centuries

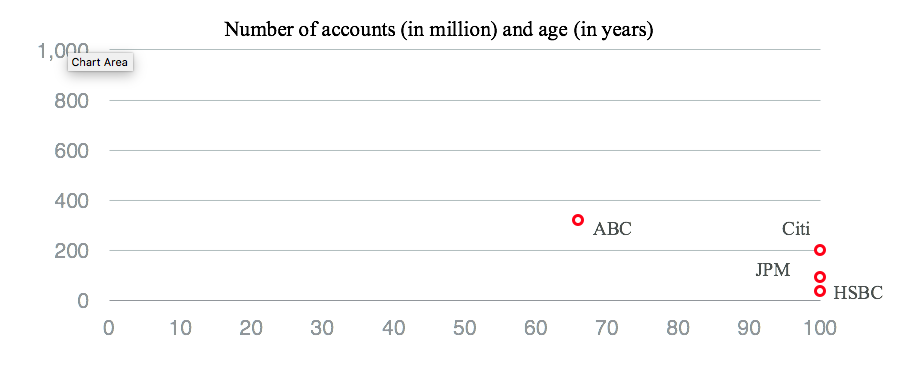

“Too big to fail” is a concept that neatly summarises the importance of traditional finance, and the scale of the largest banks, insurers and asset managers – both in terms of client base and their roles in the economy.

Looking at numbers, the biggest banks in the world have a few hundred million clients, and are more than 100 year-old. For example, Citi serves 200 million clients, and was founded in 1812. Looking at some of the fastest growing banks in the world, Agricultural Bank of China has 320m clients, and was founded 65 years ago.

The graph below shows the number of clients for HSBC, JPMorgan, Citi and ABC with a cap at 100 years so that the graph is not too stretched.

Very large banks can therefore reach a few hundred million clients, which is a process that takes from 50+ years to centuries.

- Internet companies hyperscale in 10 to 20 years

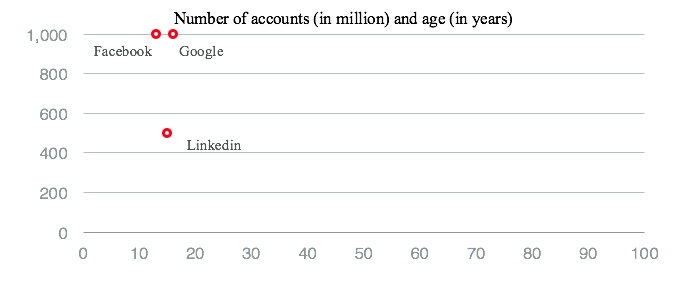

On the other hand, Internet companies do not need 100 years to reach 100m clients. Facebook for example had 1bn users in 10 years – in other words, an Internet company scales from 10x to 100x faster than a traditional financial institution. Even Linkedin, which is the smallest on the graph, has more clients than the largest banks in the world, and is only 15 years old.

Putting Facebook, Google and Linkedin on the graph, we can see a growth pattern that reaches hundreds of millions of clients in less than a decade.

This might not seem a fair comparison of course, because Internet companies:

– are not subject to strict bank regulations

– have different business models

– do not need capital

But does it mean that hyperscalability cannot happen in finance? Let’s have a look at the new players from Digital Finance, or Finance 2.0.

- Finance 2.0 companies hyperscale like Internet companies

Let’s define Finance 2.0 companies as the companies operating in finance, that were created during the last decade or so, and designed with a digital-first strategy.

There are quite a few companies that would fall in this category, and some of the most notable ones would be:

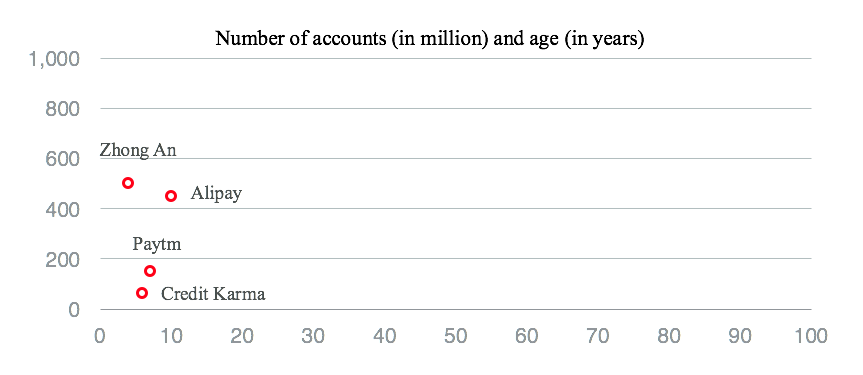

– Ant Financial / Alipay, the financial arm of Alibaba

– Zhong An, the digital insurer

– Paytm, the Indian payment company

– Credit Karma, the US credit scoring firm

Looking at their growth numbers, the most impressive is Zhong An with 500m clients in 5 years, but even Credit Karma, which is not a decade old, has more users than most banks in the world.

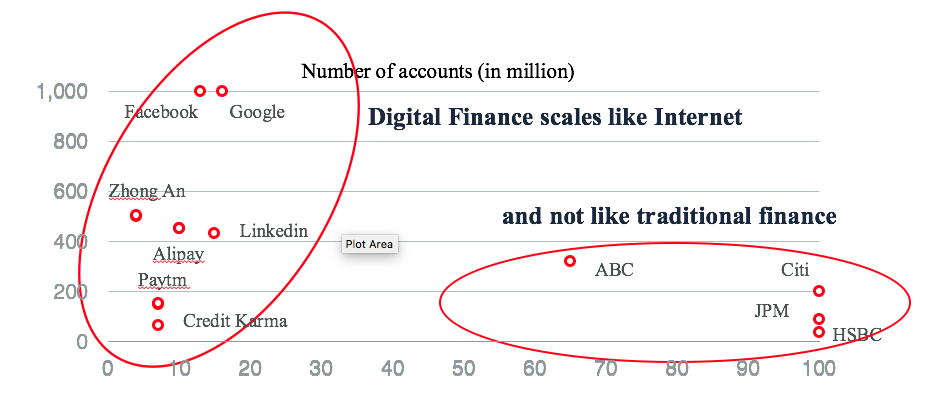

In other words, the model of hyperscalability of the Internet can also apply to finance, and this one of the most significant change happening to finance today. Because hyperscalability brings network effect, pricing power and economies of scale. And we don’t need to look further than Amazon in retail, Booking.com in travel or Google/Facebook in advertising to see how hyperscalable models disrupts industries.

If these new companies in finance were to follow the model of Internet growth, that would mean financial groups with more than a billion clients in a few years. This might sound crazy, but Ant Financial has explicitly stated that they intend to reach 2 billion users.

If we put all these companies on the same graph, we can clearly see the difference in scaling patterns between traditional finance and Finance 2.0 :

Why is Finance 2.0 hyperscalable?

What is so different between Finance 2.0 and Finance 1.0 in terms of scalability ? I think there are two main reasons:

Digital shifts cost structures from CAPEX to OPEX. Traditional finance is based on physical outlets, which means that growth tends to be linear rather than exponential. As the number of customers increase, fixed costs also increase in a linear way. This is of course a very rough approximation, but that’s not too inaccurate for retail banks. This is different for investment banking which doesn’t have the same CAPEX constraints, which is why investment banking and capital markets are so important for universal banks – but the total universe of clients is much smaller too.

On the other hand, digital growth models do not require such an increase in fixed cost, because the fixed costs are borne not by the Finance 2.0 companies, but by the infrastructure providers (Telecom Operators, Internet Service Providers).

Finance 2.0 companies can therefore grow much faster, because they don’t have to build the infrastructure as they grow, and don’t have to pay for it either.

Hyperscalable finance companies target large untapped markets. It’s not a coincidence that many of the hyperscalable finance companies are based in emerging markets where the majority of consumers do not have a bank account. These markets are very large in number – i.e. 2.2 bn people do not have a bank account – and there is little competition of existing services.

It doesn’t mean that there can’t be very fast growing companies in developed markets – i.e. Credit Karma in the US for example – but they are more likely to be in areas with less competition from traditional finance, in other words “different” products rather than “better” products.

What’s the impact of hyperscalability in finance?

Hyperscalability per se won’t have an impact in finance, because it’s just the result of a combination of factors:

– The adoption of digital finance by an increasing large proportion of the world population

– The rise of new business models and cost structures in finance

– The leverage coming from Telecom infrastructure and new technology

This results in a much faster growth in the number of clients, but what does it mean in economic terms ?

For example, assuming $8bn of net income for Citi Consumer Banking, and 200m clients, Citi makes around $40 per client. Ant Financial on the other hand, with almost $1bn of profit and 500m clients make around $2 per client, which is 20 times less. This can be explained by the difference in target clients, breadth of products and most importantly business models.

My view is that in the short-term, we’ll see the emergence of more hyperscalable companies in finance, that will acquire a very large number of clients, but with less profitability than traditional finance companies. Then as they reach a critical mass, they will expand the range of products, offer more banking-like products, and increase profitability – similarly to Facebook which quadrupled its revenues per user between 2011 and 2016.

Finance companies that can achieve hyperscalability have the potential to redesign tomorrow’s finance, but does it mean that the future is bleak for the traditional banks and insurers ? Not necessarily, because nothing prevents existing players from building hyperscalable businesses too.

Look no further than ICBC in China, which is battling with Alipay, and is now the largest bank in the world thanks to 250m clients using its mobile services.

In all cases, I don’t think that the Fintech tsunami has become an IT ripple, quite the opposite. The IT infrastructure ripple of the last few years has built the foundation for the Fintech tsunami, that will result in the emergence of massive financial groups.

If you want updates on Disruptive Finance and Fintech:

– You can enter your email address to receive an email whenever I write a new post

– You can also follow me on Twitter here

Don’t hesitate to share if you like this post