Most people who have an interest in Fintech have heard of Atom, Starling, Fidor, Mondo or Number 26. Some might have heard of Loot, or Holvi. But there is a fascinating bank that most people have never heard of, and that’s certainly because this French challenger bank doesn’t seem to seek any international visibility.

Let’s take a step back and look at the big picture for challenger banks. If I had to simplify, the objectives of challenger banks is to do to banks what Easyjet and Ryanair did to airlines and achieve the same success (from 0 to 30% market share in 10 years).

Their value proposition is equally simple: use new technologies and focus on the user interface in order to offer lower costs and a better user experience.

This, in theory, should be an unbeatable recipe for challenger banks to grab market share from traditional banks. In practice however, the benefits of “cheaper costs” and “better user experience” are rarely enough to lure consumers from their existing banks.

Which brings me to one of my favourite challenger banks: Compte Nickel. Compte Nickel is a fascinating French company to follow, not only because they are undeniably successful (200,000 accounts in less than 2 years), but also because they call into question some of the pre-conceived ideas about challenger banks.

As a large number of challengers have launched or are in the starting blocks (Fidor, Holvi, Moven, Monese, Atom, Tandem, Loot, Starling, Mondo, Number 26, Secco, etc.), the experience of Compte Nickel tells us a lot about some of the success factors in that space.

Hughes Le Bret, the CEO of Compte Nickel, very kindly accepted to share the story of his company, and this is invaluable insight for anyone interested in the future of banking.

Hugues Le Bret, CEO of Compte Nickel

Huy : Hi Hugues, many thanks for sharing your story at Compte Nickel. I find Compte Nickel fascinating, but many people outside of France haven’t heard of you. Could you tell us about you, why you launched Compte Nickel, and what was your initial vision?

Hugues : As about 40% of French people pay huge bank charges, we thought we could launch a new payment institution that would provide easy home and mobile banking services for a very fair price and help them save between €100 and €1.000 a year. As former CEO of Boursorama, the French e-Banking leader, I knew that every bank has the same strategy: to target rich consumers and cross sell savings, insurances or credit. But they usually do not target people who don’t have enough money to save or get a mortgage.

Could you tell us what is Compte Nickel? How is it different from a traditional bank ?

Compte Nickel is just like an online bank, but where no overdraft is allowed. In addition, we don’t offer credit nor savings. People can open an account, get an IBAN and receive an International Mastercard at a newsagent in less than 10 minutes.

Many challenger banks have been designed to be digital only. On the other hand, you are not – and the role of newsagents is important in your strategy. Did you consider being digital only when you started? And why did you choose to partner with newsagents instead of building your own branches?

The question is about efficiency and acquisition cost. You can’t physically get an activated payment card linked to an Iban instantaneously generated online and in less than 10 minutes. Online banks have to send their cards by post office. We reach real clients in the street and don’t spend fortunes paying lead for virtual people online. We don’t advertise. Having our own branch network wouldn’t be realistic, we needed point of sales with various products and services and a huge amount of clients every day. Ten million French people enter in a newsagent shop every day.

Account opening happens with a newsagent

Are there any metrics you could share with us? For example, the growth in account numbers? Average deposit? Primary vs. secondary accounts? Revenues? Customer acquisition costs?

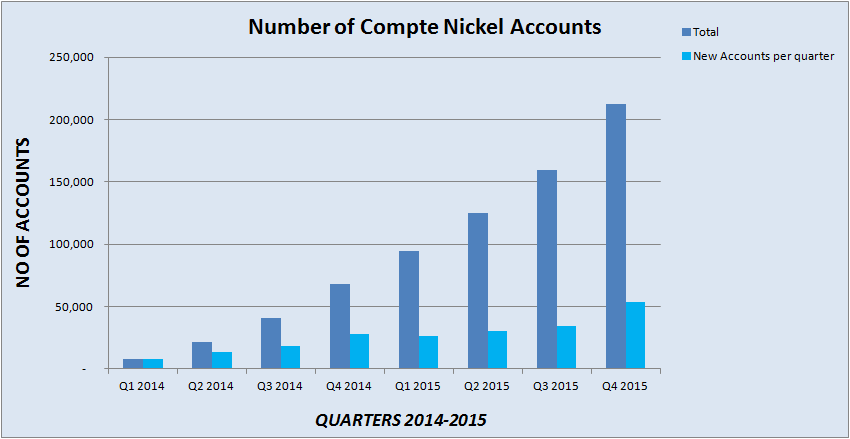

We started in February 14 and gained 4,000 customers the first month. We started 2015 with 9,000 new customers per month. As of January 2016, 18,000 new customers are joining every month. In total, our number of clients went from 0 to 213,000 in less than 2 years and our objective is to reach 35,000 new accounts per month at the end of this year.

In terms of metrics, 70% of our customers choose us as their main “bank” and receive their salaries on their Nickel account, with an average monthly flow of €1,100. 30% of them chose us for specific purpose : online payments (31% of our card payments), payment in non eurozone countries where we don’t charge a fee, etc.

Huy : How do you see the future growth of Compte Nickel? Any plans for new products or market segments?

The target for 2016 is to reach 500,000 customers by the end of the year. We will also launch an SME product this year.

Compte Nickel reached 200,000 accounts in less than 2 years, with growth picking up

In your opinion, what were the main factors contributing to the success of Compte Nickel?

We are not a full-fledged bank. People pay for a service that allows them to deposit money and make payment without any extra bells and whistles. They take control of their spendings with 100% real time payment and very detailed information, and they can’t spend more than what they have. Thanks to Compte Nickel, they save money compared to a traditional bank, and everything is super simple.

Conversely, what have been the most challenging moments you’ve had in developing the companies?

Getting the licence from the French Central Bank took 2 years and 4,800 pages! Signing agreements and SLAs with our main processing partners, raising the first € 6 million, empowering the French Tobacconist Union, opening 100 points of sale a month, all of that was also very challenging…

Thanks a lot for your answers Hugues, I’m sure we’ll continue to hear a lot about Compte Nickel!

As more and more challenger banks are launched, I suspect that many will find that having a cheaper service and a nicer UI is far from sufficient to entice consumers to switch. The example of Compte Nickel shows however that a well thought-out product combined with a clear target market and a strong acquisition strategy can be a winning proposition.

This is in my opinion the main theme this year. Until now, we haven’t seen much difference between challenger banks because it’s a very new market, but I suspect that in 2016 we will start to see a real differentiation between the challenger banks that are bringing a real value proposition to their customers – which will be easily observed in their metrics – and those that will struggle to find traction.

This is also perhaps a good symbol that such a success takes place in France, and not in the UK: although Fintech is by far the most dynamic in the UK, many interesting initiatives will happen in other countries.

If you want updates on Disruptive Finance and Fintech:

– You can enter your email address to receive an email whenever I write a new post

– You can also follow me on Twitter here

– Or add Disruptive Finance to your RSS reader

And thanks for reading. Don’t hesitate to share if you like this post!