(This is part 1 of this topic. Part 2 with the discussion results can be found here)

That will be the fascinating theme of the roundtable that I will be discussing with my fellow attendees at Money X (part of Web Summit) this week. To prepare for the conference, I’ve put together a few data points to start the dialogue – which hopefully should lead to thought-provoking views.

This is of course slightly misleading to focus only on valuation or market capitalisation as the measure of success for Fintech (for example, Wikpedia is immensely valuable, but wouldn’t appear in such a ranking). This has the merit of simplicity though, and so far most Fintech companies are commercial organisations and valuation is a good metrics to start with.

First, what are the most valued Fintech startups today? Finovate did an excellent analysis in July, and ranked the largest Fintech startups (all the data I use below are from that document, please refer to it for more info). In total, there are 84 Fintech startups, the largest being valued $10bn down to $500m.

| Company | Sector | Valuation ($ bn) |

| Lufax | Lending | 9.6 |

| Zhong An Online | Insurance | 8 |

| Square | Payments | 6 |

| LendingClub | Lending | 5.6 |

| Zillow | Real estate | 4.8 |

| Zenefits | Insurance | 4.5 |

| CreditKarma | Credit | 3.5 |

| Stripe | Payments | 3.5 |

| Powa Technologies | Payments | 2.7 |

| Klarna | Payments | 2.5 |

| Xero | Accounting | 2.4 |

| One97 | Payments | 2 |

| Prosper | Lending | 1.9 |

| Affirm | Lending | 1.8 |

| Biz2Credit | Lending | 1.7 |

| Dataminr | Analytics | 1.6 |

| Lakala | Payments | 1.6 |

| Adyen | Payments | 1.5 |

| FinancialForce.com | Accounting | 1.5 |

| Oscar | Insurance | 1.5 |

| Wonga | Lending | 1.5 |

| Zuora | Payments | 1.5 |

| iZettle | Payments | 1.4 |

| Housing.com | Real estate | 1.3 |

| Qufenqi | Lending | 1.3 |

| Revel Systems | Payments | 1.3 |

| Social Finance (SoFI) | Lending | 1.3 |

| Jimubox | Lending | 1.1 |

| Q2 | Banking | 1.1 |

| CommonBond | Lending | <1 |

| Coupa Software | Accounting | 1 |

| Fenergo | Onboarding | 1 |

| FundingCircle | Lending | 1 |

| Kofax | Doc mgmt | 1 |

| Mozido | Payments | 1 |

| TransferWise | Payments | 1 |

| Trusteer | Security | 1 |

| Vanco Payments | Payments | 1 |

| Avant | Lending | 0.9 |

| ClimateCorp | Insurance | 0.9 |

| Coinbase | Bitcoin | 0.9 |

| Dynamics | Payments | 0.9 |

| IEX Group | Investing | 0.9 |

| LendingHome | Lending | 0.9 |

| On Deck | Lending | 0.9 |

| RenRenDai | Lending | 0.9 |

| Xoom | Payments | 0.9 |

| 21 Inc | Bitcoin | 0.8 |

| BankBazaar | Banking | 0.8 |

| Betterment | Investing | 0.8 |

| Braintree | Payments | 0.8 |

| LifeLock | Credit | 0.8 |

| Rong360 | Lending | 0.8 |

| Wealthfront | Investing | 0.8 |

| Accurate Group | Real estate | 0.7 |

| App Annie | Mobile | 0.7 |

| Auction.com | Real estate | 0.7 |

| Ayadsi | Analytics | 0.7 |

| Oportun | Lending | 0.7 |

| Taulia | Payments | 0.7 |

| WorldRemit | Payments | 0.7 |

| AnJuke | Real estate | 0.6 |

| Circle Internet Finance | Bitcoin | 0.6 |

| EzBob | Lending | 0.6 |

| FangDD | Real estate | 0.6 |

| Kabbage | Lending | 0.6 |

| Bill.com | Payments | 0.5 |

| CAN Capital | Lending | 0.5 |

| Cardlytics | Marketing | 0.5 |

| Credorax | Payments | 0.5 |

| Financial Software Systems | Risk Mgmt | 0.5 |

| FreeCharge | Payments | 0.5 |

| Kreditech | Lending | 0.5 |

| Motif Investing | Investing | 0.5 |

| Ping Identity | Security | 0.5 |

| PolicyBazaar | Insurance | 0.5 |

| Radius | Marketing | 0.5 |

| Receivables Exchange | Lending | 0.5 |

| Snowball Finance | Investing | 0.5 |

| Strategic Funding Source | Lending | 0.5 |

| U51 | Lending | 0.5 |

| Wepay | Payments | 0.5 |

| VivaReal | Real estate | 0.5 |

| Zopa | Lending | 0.5 |

| Shopkeep | Mobile POS | 0.5 |

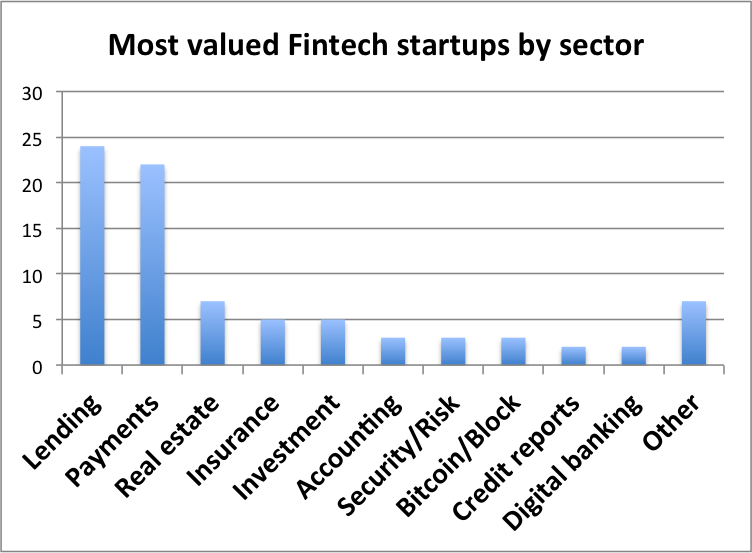

When split by sector, half of the Fintech unicorns or semi-unicorns are focused on Lending and Payments.

Source : Finovate

The list above could represent a very good starting point for some of the most valued Fintech companies in 2020. To this, I would also add a few other companies, such as Paypal and Ant Financial, both valued around $50bn. It is interesting to see that the two largest Fintech companies today are spun off from other large Internet groups – could the most valued Fintech startups in 2020 actually come from existing Internet companies?

Now, if we were to compare these Fintech startups to the largest companies in traditional finance, the list below shows the 19 largest financial providers:

| Company | Sector | Valuation ($ bn) |

| Berkshire Hathaway | Investment Company | 357 |

| Wells Fargo | Bank | 280 |

| ICBC | Bank | 275 |

| JPMorgan Chase | Bank | 226 |

| China Construction Bank | Bank | 209 |

| Bank of China | Bank | 197 |

| Agricultural bank of China | Bank | 189 |

| HSBC Holdings | Bank | 164 |

| Bank of America | Bank | 162 |

| Visa Inc | Payments | 161 |

| China Life Insurance | Insurance | 157 |

| Citigroup | Bank | 156 |

| Commonwealth bank | Bank | 115 |

| Ping An Insurance | Insurance | 113 |

| Banco Santander | Bank | 106 |

| MasterCard Inc | Payments | 100 |

| Westpac Banking Corp | Bank | 94 |

| Mitsubishi UFJ | Bank | 88 |

| Royal Bank of Canada | Bank | 87 |

In traditional finance, 15 of the largest companies are banks, 2 are insurers, 2 in payment, and 1 a holding company. This is a clear difference between Fintechs that are focused on verticals, whereas the largest traditional groups are diversified across the whole value chain. Will the largest Fintechs still be focused on niche areas or will they expand into other sectors?

Those are some initial data points for the discussion this week, and I’ll be happy to report back the – no doubt fascinating – conclusions of our group. If in the meantime you have strong views, don’t hesitate to send me a tweet.

Update: you can find the second part with the discussion results here about the most valuable Fintech companies in 2020.

Follow me on Twitter here